Australian energy has seen some interesting developments over the past few months – a new, more climate focussed and aware federal government, skyrocketing energy prices which have prompted calls for price caps or windfall profit taxes and finally the potential resurrection of the SEC in Victoria.

Surging coal and gas prices have been driven, in large part, by the Russian invasion of Ukraine. For governments in Australia this is a double edged sword, while high energy prices are putting real pressure on local households and business coal and gas export earnings are driving massive, budget repairing royalty revenues into state and federal coffers.

Figure 1 Energy price inflation. Date from the Reserve Bank of Australia (1)

About 75% of Australia’s coal and gas is exported with the balance being consumed by domestic customers. While both exports and domestic consumption are expected to decline and potentially disappear under a net zero future the timeline for each will be different. Exports could potentially continue for the foreseeable until green steel is a reality and key international partners such as Japan and Korea no longer need traditional Australian energy. The domestic requirement for coal and gas, however, is something that current and future governments will need to manage as Australia works toward the carbon reduction targets it has set itself under the Paris agreement. If the current political pressure from green and teal candidates is maintained it is quite conceivable that domestic consumption, particularly for thermal coal, falls at a faster rate than export demand. Under this scenario Australia will continue to mine coal and extract gas but will need less and less of it for its own use.

Returning to the current situation, high prices are great for export sales but are hurting domestic consumers. The magnitude of price rises is shown in Figure 1 above. The upper curves show that the Newcastle coal price has increased from about US$70/tonne in late 2020 to its current level of around US$400/tonne – a roughly 550% increase over the past 2 years. The lower graph shows the cost of gas being paid by east coast consumers and as for coal, prices are 5-6x times higher than they were 2 years ago. The LNG netback is the export gas price less the conversion cost of compression and shipping – in other words the breakeven price for sale into the domestic market relative to an international sale. This comparison supports claims that local gas consumers are paying similar prices to customers importing Australian LNG.

So what should the federal government do? They have committed to reducing pressure on Australian businesses and households but have not yet announced what they will actually do. One option is setting a price cap on gas at around $12/GJ – less than a third of the current international market. This will provide relief for gas consumers who are currently buying gas on the “spot” market (the short term daily price). Coal is a bit different as it is typically sold to power companies under longer term supply contracts. Capping coal prices would therefore require modifying existing contracts, raising questions of the legal mechanics and compensation. Another approach is to impose a windfall tax on coal and gas producers and use this revenue to compensate energy consumers. The net impact of which would probably be a convoluted version of a price cap but could overcome some of the issues associated with existing supply contracts. Both approaches would create a subsidy for the local market which represents a significant shift away from both the “export parity pricing” principle introduced way back in the 1970s (2) and the open market, free trade position that has long been an established part of Australia’s international trade stance.

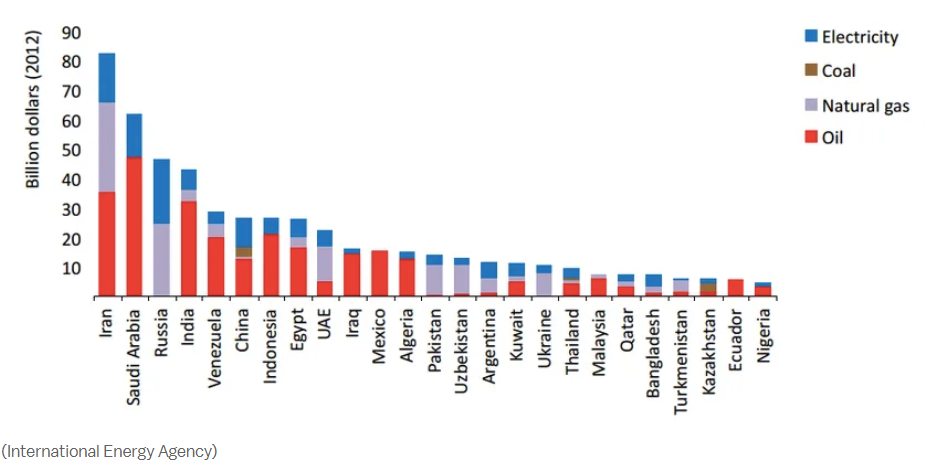

Overt subsidies for fossil fuels are opposed by both neoliberal global trade advocates and climate activists (3,4,5,6,7,8). The motivation for green groups is that they see subsidies encouraging and supporting the fossil fuel status quo to the detriment of new low carbon and renewable energy investment. Anti fossil fuel advocates categorise subsidies as either production or consumption subsidies. The former reflects claims that fossil fuel producers are not made to account for the health and environmental impacts associated with the extraction, processing and use of fossil fuels. The latter are schemes in which fossil fuels or electricity produced from fossil fuels are made available to local markets at prices below market. Australia is obviously currently considering implementing a consumption subsidy, though advocates will claim Australia already employs a range of pro fossil fuel production subsidies. Some estimates of global fossil fuel subsidies are shown in the figures below.

Figure 2 Estimates of global production (implicit) and consumption (explicit) subsidies (3)

Figure 3 Consumption subsidies in a range of energy producing nations (4)

While consumption subsidies – selling below market – are reasonably easy to quantify, production subsidies are much more subjective. They require both an estimate of the higher rates of illness or the level of environmental damage as well as an implied cost assumption for these negative outcomes. As mentioned above the main goal is often less about producing a robust auditable figure than to highlight the significant and often discounted costs that are claimed to result from the production and use of fossil fuels. Criticism of fossil fuel subsidies was very common a decade ago when renewables were more expensive than fossil fuels (particularly coal) and that drawing attention to the “real” cost of coal based generation was useful in making the transition to wind and solar look more financially logical. While this argument has been less important in recent times as wind and solar has become dramatically cheaper, there is no doubt that climate activists remain opposed to anything that looks like a subsidy for fossil fuels.

Given there is ideological opposition to fossil fuel subsidies on both sides of the political fence – especially overt financial subsidies – is this influencing the current federal government’s thinking? Surprisingly, opposition to the idea of subsidised gas and coal has been pretty muted, although the Greens are arguing in favour of a windfall tax – perhaps thinking that the tax could be expanded to cover export sales – while business groups are concerned that this sort of government involvement will damage Australia’s reputation as a reliable supplier.

Other views on the topic include state governments who have adopted different positions depending on whether they are a net importer or exporter of gas and electricity. Queensland, which is both a major coal and gas producer as well as the only state that still has state owned generation assets, is pushing strongly for federal compensation for any lost state revenue. Together with South Australia, Queensland is also calling for NSW and Victoria to increase gas drilling and add additional supply into the domestic market. The call for increased supply is echoed by pro-business groups and especially gas producers though this is more an opportunistic criticism of restrictions in NSW and particularly Victoria than a suggestion that will potentially reduce prices in the next 12 months or so.

At a headline level it seems that a pragmatic approach is winning the debate. The financial impact of steeply higher electricity and power costs on low income households is clearly a real issue. Additionally there is a not unreasonable presumption that the current situation is an anomaly caused by an artificial external event meaning government intervention can be justified without representing either long term support for fossil fuels or a radical change in trade policy. As always with climate and decarbonisation, however, there is underlying detail worth exploring, highlighting that not only is coal different to gas but household customers are often different to large industrial users.

Abnormally high coal prices impact consumers via higher electricity prices – domestic and industrial consumers for the most part don’t buy coal, they buy electricity. Gas is much more complex. Not only is gas also used to generate electricity but it is bought by households for home heating and cooking and by large industrial customers as either an energy source or a raw material (or both). The future need for gas is also more complex than for coal. While deep decarbonisation inevitably means a complete phase out of domestic coal based electricity the same is not necessarily the same for gas. Unsurprisingly, green groups want to see gas following the coal trajectory but other studies (9) highlight the potential for gas well past 2050. This would be both for back up power generation and in industries where a low carbon pathway is not yet clear.

How does a potentially different future for coal and gas impact the current debate? At the level of providing short term relief to struggling households there is no real connection but it is a sign that the new federal government is being slowly drawn into the quicksand of managing and planning for a net zero future. Does the government have a view on the medium term role for gas? One suspects the party has multiple but not an agreed position. This means it does have a view on how much domestic gas will be needed in a decade or two and who might need it. State governments have staked out different positions which will need to be navigated by the Albanese government. Victoria and to a lesser extent NSW are opposed to new gas extraction while Queensland and South Australia are much more supportive. This obviously cuts across traditional major party positions as do underlying tensions between pro manufacturing unions and climate sensitive inner city voters.

Of greater relevance to the current debate, there are also significant differences between domestic and large scale industrial customers. Households are price takers and if electricity and gas prices spike by four or five times there is very little they can do other than cut back elsewhere – if they have the capacity to do so. Given the magnitude of increased energy prices some level of support is clearly warranted – at least for low and middle income families.

Industrial consumers, on the other hand, are currently dealing with the same higher gas and electricity prices as much of the rest of the world. Without criticising companies for asking, government funded price relief should really be restricted to consumers who can show solid evidence of decreased competitiveness. This is especially the case where consumers are large enough to be able to negotiate the terms and conditions of their gas supply – if they have opted to take spot pricing rather than lock in long term pricing they made a commercial decision that has backfired. Should they now be bailed out by the government?.

Additionally, variations in cost inputs is something the management teams of large scale industries are paid to deal with. A range of gas and potentially electricity hedging options designed specifically to deal with unexpected price movements will have been available for many of the consumers now calling for price relief. Once again this is asking for government support to cover a failure to take prudent risk mitigation precautions.

Taking too hard a line with companies who are at least partially to blame for finding themselves in financial distress risks the politics of seeing workers losing their jobs and taking the hit for management actions (or inaction). Some testing decisions will need to be made over the next week or so.

If there is a reasonably rapid conclusion to the situation in Ukraine, global coal and gas prices will return to normal. If so, measures to reduce energy prices will theoretically be rolled back – an outcome that is certainly not inevitable – and the current debate will fade away. What won’t fade away, however, is ongoing tensions between a short term reliance on coal and gas and a medium term, low carbon future that will almost inevitably still need some level of fossil fuel supply – especially gas.

That brings us to the final recent development – the announcement by the newly elected Andrew’s government to recreate the government owned State Electricity Commission (SEC). While there are few details on the new entity, it will apparently be 51% government owned entity and looking to l spend $1 billion to build 4.5 GW of new renewables. The promise of a more rapid transition to renewables with all profits being retained and reinvested in the Victorian grid has obvious appeal but one wonders if direct government involvement is needed elsewhere. While investment in wind, solar and batteries is critical to achieving net zero this should be the easy part given that existing coal generation is closing and wind and solar is the low cost alternative. As discussed above, what is likely to prove more challenging over the next few decades is managing both the decline and shutdown of coal based power plants as well as working out if gas is going to be phased out or needed in a backup role to cover shortfalls in renewable output.

As the nation transitions to zero carbon, domestic coal and gas assets – power plants, pipelines and high voltage lines will effectively become a hedge or insurance against shortfalls elsewhere in the system. They will be less a source of profit than a cost that must be borne while a grid based on renewables and batteries is developed and proven robust. It is not obvious how this can be attractive to private ownership – at least without a completely new compensation model.

If the public ultimately needs to backstop ageing and increasingly unloved coal and gas then one option may be to take them over. In an ideal world this will ensure critical maintenance is done, price spikes are smoothed over, operation can be restricted to periods when power output is needed and the government will have an incentive to maximise the reliability of non fossil generators.

We may now be starting to see the arc of debate changing – from one where challenging the incumbency, dominance and “true” cost of fossil fuel generation was a useful narrative to one that recognises these assets cant be simply shut down, they will need active and skillful management to make sure they remain viable as they are gradually retired. This may be a more valuable role of a revamped SEC than competing with private investment to build out new renewables and hydrogen production and infrastructure. The new federal government and their more well established Victorian colleagues have full terms ahead of them – both will find the pressures to decarbonisation becoming increasingly urgent and potentially also requiring some flexibility and innovative thinking as 2030 targets get closer and closer

- https://www.rba.gov.au/publications/smp/2022/aug/box-a-recent-developments-in-energy-prices.html)

- https://www.abc.net.au/news/2021-10-29/record-prices-are-at-record-highs-fraser-government-john-howard/100575924

- https://www.imf.org/en/Topics/climate-change/energy-subsidies

- https://www.iea.org/topics/energy-subsidies

- https://www.greenpeace.org.au/blog/fossil-fuel-subsidies-a-waste-of-taxpayers-money/

- https://australiainstitute.org.au/post/australian-fossil-fuel-subsidies-surge-to-11-6-billion-in-2021-22/

- https://reneweconomy.com.au/global-fossil-fuel-subsidies-rocket-to-almost-us700-billion-in-2021/

- https://www.vox.com/2015/1/29/7945525/fossil-fuel-subsidies

- https://energy.unimelb.edu.au/news-and-events/events/net-zero-australia-interim-findings