Global gas prices have risen dramatically in the last 12 months. Gas pricing is important not just because it is a key input to many industrial processes but because gas effectively sets the price of electricity, which is also surging to unprecedented levels in some countries. High gas prices also impact individual households where it is used for domestic heating as is the case across much of Europe. The current period of high gas pricing will therefore be literally life threatening as the northern hemisphere winter approaches.

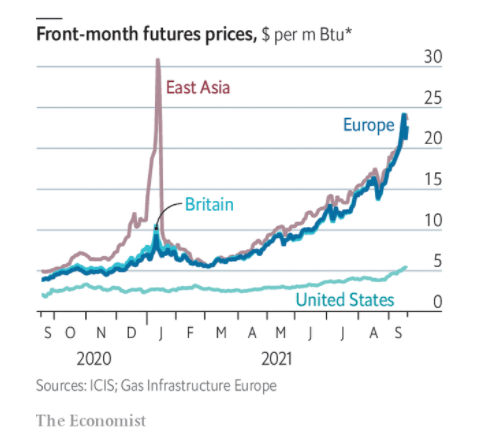

Figure 1 – Increasing gas prices in US$ per Million British Thermal Units (1)

The graph above shows that European prices, at almost $25/MMBtu, are about 5 times higher than a year ago. As with any market dislocation there are a myriad reasons, both short term and more structural, for the current situation. Europe and many parts of Asia have limited domestic production and rely on exporting nations to supply this shortfall. Key gas exporters are Russia (via pipeline into Europe), Qatar, Australia, Norway, Canada and in more recent times the US. The figure above allows a comparison between gas importers and those with adequate domestic production. While the self-sufficient US has seen a modest rise in pricing, its consumers are paying far less for their gas than businesses and households across both Europe and Asia.

The current price spike will eventually ease (or so the pundits tell us), perhaps after Russia gains European approval for its Nord Stream 2 gas pipeline. Assuming this happens and things return to something closer to normal, what will be the impact on climate politics and what might be the lessons from the last 12 months?

Talking points for advocates

The current gas crisis plays to well established talking points. Increasing fossil fuel prices has long been the goal of environmental groups who believe society does not adequately recognise the cost of environmental damage and health impacts associated with the use of coal, gas and oil. With this logic higher prices for fossil fuels might represent short term pain but forcing consumers to pay what they regard as the true cost of fossil fuels will accelerate the transition to cleaner energy.

Countering this world view are arguments conflating high energy prices with economic damage. The current European crisis is being used by conservative commentators as evidence that an overly aggressive green revolution will make energy unaffordable and destroy the economy.

Between these extremes, more moderate observers will probably start to reconsider the popular narrative that wind and solar are now so cheap that decarbonisation will inevitably lead to declining energy prices. It now looks more likely that there will be volatility during the transition away from fossil fuels.

With the Glasgow climate meeting only weeks away, one wonders if familiar talking points from familiar commentators will change many minds. It is more likely that most nations are by now committed to at least a partial transition to zero carbon energy. While some are more committed and are dealing with the challenges more successfully than others it would be more than surprising if the current gas spike forced a major global rethink. If we are lucky, however, it may push lawmakers to take a harder and more pragmatic look at their energy transition plans and especially at the safeguards and contingency plans they should have in place.

Domestic heating. At a household level high gas prices may drive residents in Europe and perhaps in Asia as well to re-evaluate the technology they use to heat their homes. Across Europe the most common form of domestic heating are gas boilers. In the UK, for example, 85% of homes are heated with gas (2) and in the current environment this is creating real issues for low income groups. There are, however, alternatives. In Scandinavia, where home heating is clearly essential, heat pumps have increasingly become the preferred option. Heat pumps, which are based on the thermodynamic principles used in refrigeration, don’t run on imported gas and rely instead on electricity. For countries such as Sweden, whose electricity grid is made up of hydro, nuclear and renewable generation, the use of heat pumps both reduces exposure to international gas markets and helps minimise national GHG emissions.

In addition to decisions by individual homeowners, governments across Europe and Asia may see the current gas pricing spike as an ideal opportunity to promote heat pumps or other non gas based, low emissions heating systems. Decarbonisation of home heating will be required to meet net zero targets and as has been shown with rooftop solar, subsidies and other inducements can be very effective in encouraging the roll out of green technology.

Figure 2 Growth in Swedish heat pump usage over the last two decades

Gas supply chains and promoting Hydrogen. In addition to home heating and power generation, gas plays a key role in many industries, either as an energy input or a feedstock. These industrial applications will decarbonise at different rates and in some cases zero carbon may not be possible. Given that gas consumption, even if it is on a declining trend, remains an economic necessity, companies and governments will need to give more attention to securing long term supplies. This is obviously an easy call to make in the middle of a supply driven price spike but one lesson for central governments may be that the rhetoric around an inexorable decline in demand for fossil fuels may have been exaggerated and fossil fuels will continue to be vital energy input even if the overall demand trajectory is down. It will prove more expedient to err on the side of higher than expected national fossil fuel consumption than the converse.

Increased promotion of hydrogen as an alternative for gas also requires more urgent attention. For some nations this will mean working to create a domestic production capacity while for others it will be looking at import supply options. Where hydrogen is not an option this should be reflected in national plans – planning for a miracle is to be discouraged.

Where industrial gas to hydrogen conversion is feasible it is currently stymied by the politics of grey, blue and green hydrogen. Climate zealots refuse to countenance anything other than hydrogen produced by electrolysis using 100% renewable electricity. In Australia, Alan Finkel (3) has suggested kick-starting the hydrogen supply chain by initially using grey and blue hydrogen before shifting fully to the favoured green version.

A response to the current gas shortage might be to realise that industry wont, and indeed can’t, shift from gas to hydrogen without either subsidies or a guaranteed low cost hydrogen supply. Governments may need to help create this supply – accept grey or blue hydrogen as an interim step, set aside renewable generation for hydrogen production or cover the cost difference between gas and hydrogen as well as helping with the required capital modifications.

Partial replacement of gas with hydrogen, just like the electrification of home heating, ultimately needs to happen to get to net zero world so there is a strong argument, perhaps as a result of the Glasgow meeting, for national governments to become more actively involved now in programs that support these end goals.

Electricity generation As mentioned above gas is also used for power generation and, as shown in Figure 1, escalating gas prices are feeding in electricity pricing. In the short run this is to be expected as gas provides 20% of total European electricity and over 40% in the UK, the Netherlands, Italy and Ireland.

Figure 3 European Power by Generation Source (4)

Gas and to a lesser extent hydro are likely to be the swing generators in the overall European grid. Coal and nuclear, which supply 42% of generation, are more suited to constant, baseload operation while wind and solar, which only contribute 17% of total generation are not suitable for demand following unless paired with appropriate storage. In the lexicon of the electrical grid, gas is on the margin (supplies the margin GWhour) and hence sets the price.

Looking at the current makeup of power generation in Europe, one gets a sense of the energy transition occurring across much of the globe. The grid in many countries was based on large scale base load fossil fuel (or nuclear) plants supported by fast acting gas plants. Over the past decade or so this configuration has been flexible enough, especially when interconnected into larger regional grids, to incorporate significant levels of renewables without too much drama. This is beginning to change. As the base load plants are being closed and generation becomes more reliant on wind and solar, the grid is becoming a transitory hybrid, not representative of either the original design or the future vision. The ability of this part baseload/part renewable configuration to reliably produce cheap electricity will be problematic if emergency generation capability, typically requiring gas, is neglected or long term power storage options are not prioritised.

If the mirage of a smooth, problem free transition from coal and gas based generation to renewables has been shaken, what might national governments do in response? This will vary across the globe depending on the political stance of parties in power and the make up of individual power sectors but there will be some common themes

Nuclear Capacity. One suspects that the value of baseload, zero carbon nuclear power has been enhanced. Aside from the odd nuclear engineer, no-one really likes nuclear but it is carbon free, it can run independently of the prevailing weather and does not require regular fuel deliveries. In addition fuel is a relatively small part of the running costs of a nuclear plant so a fuel price spike is typically no big deal.

Figure 4 The global nuclear fleet which produces 10% of global electricity (5)

As shown in Figure 4, global nuclear generation has been relatively stable for the last decade or so and recent events may mean that this remains the case in the foreseeable future. Maybe the nuclear fleet will eventually become obsolete but not until a successful transition to renewables is proven in reality as well as on a spreadsheet.

Storage – especially long term storage. Making sure electrical supply can meet expected and actual demand is becoming more complex. Weather and climate have always impacted demand – more air conditioning in the summer and increased heating in the winter. As more renewables are added, supply also becomes climate dependent – ample generation on windy summer days and a potential shortfall when the days are short, cloudy and still. This is where the need for storage comes in. Excess power generated when the conditions are favourable needs to be stored for times when supply is not so robust.

Media attention seems to focus on short term storage – lithium ion “big batteries” that can discharge over a few hours or perhaps a day at most. These are useful, particularly when paired with solar generation but would not have helped in the current gas squeeze. What all nations who will rely on renewables need is long term storage capable of discharging over weeks and potentially months. This sort of storage could have been used to support the European grid, allowing gas to be saved for critical winter heating. Currently pumped hydro is the only proven storage long term storage technology but various forms of flow batteries are being developed for this application.

Expect to see a greater focus on long term storage, potentially requiring storage as a permitting precondition for new renewable generation. The national discussion, which often fixates on the percentage of renewable generation, should articulate the national long term storage goal. For example, Australians should know that they will eventually need 15 GW of long term storage capable of continuously delivering 12,500 GWhours.

Demand flexibility Traditional grid operation has typically treated demand variability as a given and worked to ensure that supply was available to meet whatever was required. Only in exceptional circumstances would governments or regulatory authorities ask for demand restraint to prevent blackouts. That paradigm may need to change.

One obvious area is to maximise the amount of rooftop solar paired with household battery systems. This could be used to flex the demand on the grid when supply is short. The same principle could be applied to some commercial operations, for example warehouses and retail outlets. This won’t happen without subsidies, well designed systems and especially pricing signals that incentivise and inform owners how to best use the power they have generated and stored. This is not a new suggestion but the current focus on gas and power pricing volatility is an ideal time to look at addressing the massive imbalance between distributing solar generation and storage.

In parallel, low income households will need to be identified and sheltered from the impacts of high costs or limited supply. One approach would be to make it financially attractive for wealthy consumers to leave the grid when supply is short making it easier to supply those who have no option but to rely on the grid.

Net Zero and Gas back up generation As it becomes clearer that there will be bumps in the road to 100% zero carbon electricity, it is more likely that we will see gas generation assets kept as an insurance backup. Gas plants are technically ideal for this purpose – easy to start up and shutdown and able to be kept on standby for extended periods. Gas is also the lowest emitting fossil fuel so while keeping some gas in the mix will generate GHG emissions these will be lower than coal or diesel.

Obviously the current gas pricing environment is not the result of a lack of gas generation but as elected officials review the economic and political fallout of failing to guarantee sufficient power to their voters they should be thinking of other scenarios where they will be exposed.

An aspect of net zero carbon targets that doesn’t get much air time is what level of negative emissions are anticipated and hence what level of residual emissions can be tolerated. Climate activists won’t much like this logic, arguing for zero emissions on an absolute basis with any negative emissions helping to mitigate past excesses. A more practical response, at least until a 100% renewables grid is demonstrated over several decades, is to consider gas as an emergency back up. This will particularly be the case in highly populated regions like Europe and Asia where large scale pumped hydro storage is not feasible and lithium Ion batteries can’t provide the depth of required storage.

It will be interesting to see if the suggestion of using gas in a back up insurance role, restricted by carbon taxes from being used outside this purpose, gains traction. If so it’s demonisation by more zealous climate activists will be seen as irrelevant or counterproductive.

Conclusion

The current focus on European energy prices reflects that volatility and black swan events are a reality of life, especially with a global transformation in energy supply. The next “crisis” won’t be the same as the current situation but inevitably there will be common themes.

Dislocation of energy markets have an impact on individuals and households and not unreasonably attract media attention. They also attract the activist community and are used to support and reinforce entrenched and familiar positions. Hopefully there is a longer term perspective that takes a closer look at some of the issues outlined above.

Making sure that economic safety nets for low income families are in place and working is a priority and where this is not the case elected officials should be hurrying to remedy the situation. An acceptance that fossil fuels will continue to be used for decades, albeit in decreasing amounts, should be an important lesson and drive work to make sure that supply chains and surge capacity are kept in robust working condition. In combination with the climate focus created by the Glasgow meeting, the current gas price surge should prompt more detailed scenario planning – replacing what can currently be simply summarised as “replace coal with renewables” and hope for the best.

There will be noise and commentary from activists but as fossil fuel plants shut and investment in supply declines the world will become ever more reliant on renewables. This is unlikely to be a smooth process and governments and regulatory bodies will be well served creating some space and independence from activists on all sides of the energy debate. Voices from the sidelines will not be held accountable for the plans they promote or the forecasts they make.

- https://www.economist.com/graphic-detail/2021/09/20/what-is-behind-rocketing-natural-gas-prices

- https://ec.europa.eu/energy/content/space-heating-heterogenous-among-european-countries_en

- https://www.chiefscientist.gov.au/news/hydrogen-australias-future

- https://ec.europa.eu/eurostat/databrowser/view/NRG_BAL_C__custom_938495/bookmark/table?lang=en,en&bookmarkId=3dd894c7-087c-418e-aa27-1e5945f5c705

- https://world-nuclear.org/information-library/current-and-future-generation/nuclear-power-in-the-world-today.aspx