The Australian Electricity Market operator (AEMO) is a public/private entity charged with managing the nation’s key energy markets. This includes the National Energy Market (NEM) which is the integrated electricity grid covering all Australian states with the exception of Western Australia and Northern Territory. Management of the NEM is underpinned by state and federal law and includes functions such as monitoring and approving outage schedules, advising generators on short and medium term supply/demand balances and working with major generators (and customers) to ensure that there is both sufficient supply available given potential transmission constraints to meet demand and that generation comes from the lowest cost sources (1).

AEMO was a creation of the Council of Australian Governments (COAG) and is funded by charges levied on electricity (and other energy) transmission. AEMO is not an advocacy or lobby group and in theory represents the voice of independent, technical expertise.

In July AEMO published an ‘Integrated System Plan’ (ISP) (2) that “identifies investment choices and recommends essential actions to optimise consumer benefits as Australia experiences what is acknowledged to be the world’s fastest energy transition. That is, it aims to minimise costs and the risk of events that can adversely impact future power costs and consumer prices, while also maintaining the reliability and security of the power system”

In other words the ISP examines what grid infrastructure investment is needed between now and 2040 to ensure the NEM continues to generate reliable, low cost power while meeting current and potential new government emission reduction and renewable targets. Note that Australian’s current emission and renewable targets are typically regarded as relatively modest by global standards.

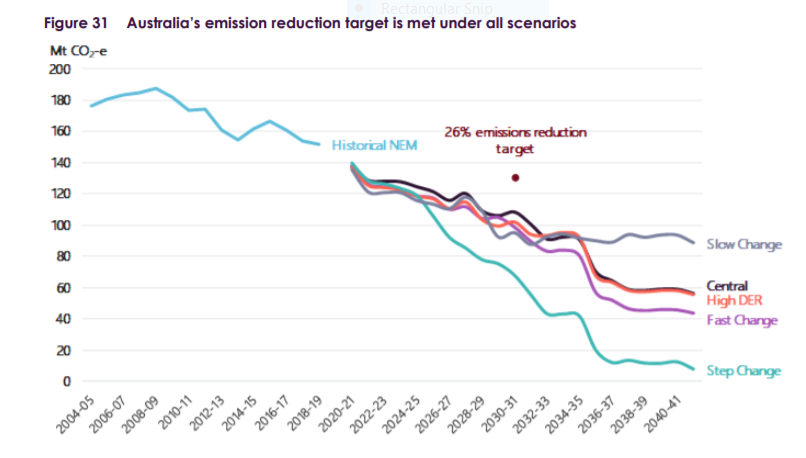

So what does AEMO think the NEM will look like in 2040 if investments are optimised to lowest cost, reliable generation while also meeting current policy settings? From an emissions intensity perspective, AEMO’s ISP report suggests that the NEM will produce far fewer emissions over the next 20 years as shown in Figure 31 of the ISP (reproduced below).

The different curves in Figure 31 relate to different scenarios – the “Central” scenario is based on predicted, least cost, market based investment outcomes driven by current federal and state government policies. AEMO is therefore suggesting that with existing government policy settings emissions from Australia’s electricity sector will decline by 60% through 2040. This suggests the electricity sector will do a lot of the heavy lifting if Australia meets its 2030 Paris target of a 26% emissions reduction. What drives this outcome? In simple terms, new, low cost renewables replacing aging coal plants.

So what are the other scenarios shown in the Figure above?

The “Slow Change” scenario envisages a lower level of climate ambition at a public or government level combined with a slow down in low carbon technology development. Both of these currently seem unlikely but some analysts may make the case that a corona recession could lead to a low level of infrastructure investment. Even were this to become a future reality there would still be a 50% decline in emissions from the generation sector.

Emission reductions under the “High DER” and “Fast Change” scenarios are similar to those under the “Central” scenario. The difference between these three scenarios is that the “High DER” (High Distributed Energy Resources) is based on a surge of consumer led investment in rooftop solar and electric vehicles while “Fast Change” relies more on a technology led transition with greater investment in large, utility scale generating infrastructure.

The most aggressive scenario is ”Step Change” which assumes both strong consumer and technology drivers as well as more climate friendly policies at state, federal and global levels. In contrast to the “Central” case which still retains 37% of the current coal fleet, the “Step Change” scenario has coal fired power being completely eliminated by the mid 2030’s and the grid being effectively fully decarbonised by 2040.

The table below provides an insight into the amount of new renewable generating capacity (in GW) added under each scenario. The NEM currently has about 24 GW of renewables so three of the scenarios modelled by AEMO have this increasing by 150 – 200% and under the most aggressive scenario by 300%. In summary lots more wind and solar and a lot less coal.

Incremental Renewable generating capacity (GW) by 2040 for each of the AEMO scenarios

So what should we take out AEMO’s ISP report? If we assume AEMO is an unbiased, technology neutral organisation that has as good an insight into what the future of the Australian grid as anyone, then it seems the report is telling us that decarbonisation of the power sector is basically inevitable. Granted, this will require continued community and political pressure as well as future improvements in low carbon generation technologies but both of these seem a pretty sure bet. Assuming this logic is becoming obvious to political and advocacy groups, one should expect to see a shift in how different groups position themselves for future climate and decarbonisation debates.

One obvious shift is to see political support for new coal plants should quietly fade away, perhaps leaving discussion over the role of natural gas as a contentious issue. Everyone loves a winner so expect to see everyone, including past opponents, celebrating new investments in renewables and pushing for streamlined permitting so Australia’s natural resources can be swiftly harnessed to meet the growing demands of the nation. One potentially contentious issue on the horizon is the role of pumped hydro for electricity storage. The technology itself is fairly benign but it has a large physical footprint with lots of scope for NIMBY pushback.

As has been discussed previously in this blog (3) reactions to the Finkel hydrogen strategy are showing signs of splitting along established left/right political lines. One hopes that a more bipartisan approach might evolve but perhaps that is not the natural order of political discourse. If hydrogen becomes a headline topic it will be interesting to see how the minor parties position themselves – the Greens will probably be opposed but centrist independents and even One Nation might decide it is something they can support. Finkel sees the potential for an early entry into hydrogen as a way to soften the blow from an inevitable loss of international coal markets but as yet none of the major parties has been willing to show much support for this pretty reasonable line of logic.

Finally there is the electrification transportation fleet. Australia’s uptake of electric vehicles remains very low by world standards but it is growing. Surprisingly for such a key part of the decarbonisation picture, promotion of EVs has not received the attention or emotion associated with the electricity sector. Obviously EVs need low carbon electricity to move the needle but given this is happening we will surely start to stronger demand for action on a EV rollout strategy.

Electrification of the light vehicle market remains somewhat apolitical in Australia. At the last federal election liberals did try to win votes by protecting the “tradie ute” from a forced conversion to battery power but this seems more like a throw away line in the heat of a close campaign. Labor and the Greens are more naturally supportive of EVs but this has not translated into real action. At the end of 2019 the progressive ACT government only owned 28 fully electric vehicles despite identifying up to 600 government vehicles suitable for replacement by EVs (4). This is not a strong demonstration of leadership by example.

As the AEMO conclusion that electricity is going green starts to sink in, political parties and advocacy groups have the opportunity and challenge to reset. We should be hearing more about the roll out of recharging facilities, investment in hydrogen and most problematically for rural Australia a reduction in global demand for beef, lamb and pork.